For report in pdf pdf_link

For notebook notebook

The aim of this project is to perform an in-depth analysis

assosiated with the assumptions of Modern Portfolio Theory

and how financial assets interact within the portfolio using sttistical

methods

Harry Markowitz introduced the mean-varinace

portfolio selection theory in 1952.Since then the Modern Porfolio theory

is cornerstone in the field of modern finance

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

import requests

sns.reset_defaults()Twelve stock quoted on NYSE are used for the purpose of analysis.

The data is between the period of 1st January 2008 to 31st December

2017. The data is downloaded using Twelvedata API in the

json format. The stocks are divident adjusted

| Company | Symbol |

|---|---|

| Apple Inc | AAPL |

| American Express Co | AXP |

| Boeing Co | BA |

| General Electric | GE |

| Johnson & Johnson | JNJ |

| JPMorgan Chase & Co | JPM |

| Coca-Cola Co | KO |

| McDonald’s Corp | MCD |

| Microsoft Corp | MSFT |

| Verizon Communications Inc | VZ |

| Walmart Inc | WMT |

| Exxon Mobil Corp | XOM |

# dowloading data using twelve data api

tickers = ["AAPL", "AXP", "BA", "GE","JNJ", "JPM", "KO", "MCD", "MSFT", "VZ", "WMT", "XOM"]

api_key = "*************************************"

interval = "1day"

start = "2008-01-01"

end = "2018-01-01"

stocks = []

def stock_data(tick):

url = f'https://api.twelvedata.com/time_series?symbol={tick}&start_date={start}&

end_date={end}&interval={interval}&order=ASC&apikey={api_key}'

data = requests.get(url).json()

return data["values"]df = pd.DataFrame()

df["datetime"] = pd.DataFrame(stock_data("AAPL"))["datetime"]

for tick in tickers[:6]:

df[tick] = pd.DataFrame(stock_data(tick))["close"]for tick in tickers[6:]:

df[tick] = pd.DataFrame(stock_data(tick))["close"]# datetime as index

df["datetime"] = pd.to_datetime(df["datetime"])

df.index = df["datetime"]

df.drop(["datetime"], axis=1, inplace=True)df.head()| datetime | AAPL | AXP | BA | GE | JNJ | JPM | KO | MCD | MSFT | VZ | WMT | XOM |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008-01-02 00:00:00 | 6.95857 | 51.04 | 86.62 | 282.769 | 65.91 | 42.17 | 30.545 | 58.1 | 35.22 | 40.3385 | 46.9 | 93.51 |

| 2008-01-03 00:00:00 | 6.96179 | 50.41 | 86.98 | 283.077 | 65.93 | 41.88 | 30.865 | 57.93 | 35.37 | 40.5253 | 46.38 | 93.83 |

| 2008-01-04 00:00:00 | 6.43036 | 49.14 | 85.82 | 277.231 | 65.84 | 40.93 | 30.925 | 57.05 | 34.38 | 39.7691 | 45.72 | 92.08 |

| 2008-01-07 00:00:00 | 6.34429 | 49.36 | 82.87 | 278.308 | 66.86 | 41.34 | 31.655 | 58.03 | 34.61 | 40.4692 | 46.56 | 91.22 |

| 2008-01-08 00:00:00 | 6.11607 | 47.95 | 79.91 | 272.308 | 66.94 | 39.7 | 31.785 | 57.08 | 33.45 | 39.1996 | 45.97 | 90.05 |

# any na values

df.info()<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 2518 entries, 2008-01-02 to 2017-12-29

Data columns (total 12 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 AAPL 2518 non-null object

1 AXP 2518 non-null object

2 BA 2518 non-null object

3 GE 2518 non-null object

4 JNJ 2518 non-null object

5 JPM 2518 non-null object

6 KO 2518 non-null object

7 MCD 2518 non-null object

8 MSFT 2518 non-null object

9 VZ 2518 non-null object

10 WMT 2518 non-null object

11 XOM 2518 non-null object

dtypes: object(12)

memory usage: 255.7+ KBdf.isna().sum()AAPL 0

AXP 0

BA 0

GE 0

JNJ 0

JPM 0

KO 0

MCD 0

MSFT 0

VZ 0

WMT 0

XOM 0

dtype: int64df = df.astype("float")We calculate the daily change in prices of stock using the given formulae

$$r_{asset} = \frac{P_t - P_{t-1}}{P_{t-1}}\times100$$

where

Pt is present value of adjusted close price of individual stock

Pt − 1 is previous day adjusted close price of individual stock

rasset daily return on assest

df = df.pct_change().dropna()

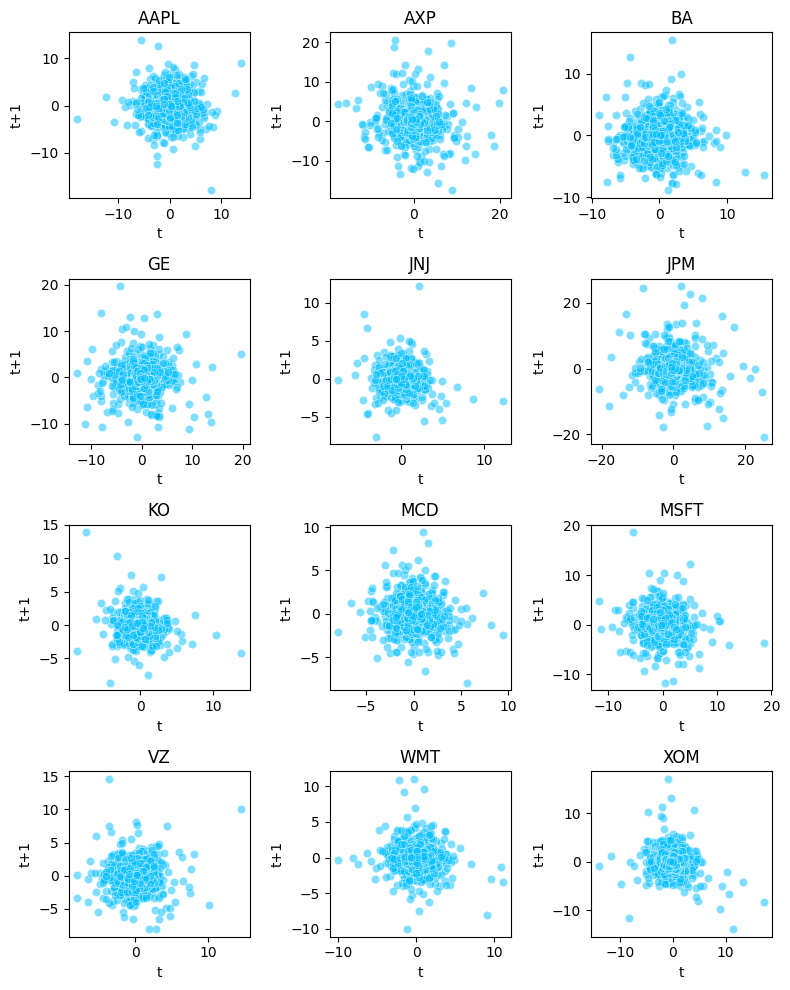

df = df*100According to Random Walk Theory stock price change

are independent of past movement trends and therefore next day price

cannot be predicted from previous price changes

We plot a simple scatterplot for our twelve assets

where we compare the previous day return against the present value and

it shows absolutely no correlation for any of the assets

which proves the assmption to be true

fig, axes = plt.subplots(nrows=4, ncols=3, figsize=(8,10))

tickers = df.columns

x = 0

for i in range(4):

for j in range(3):

ax = sns.scatterplot(x=df[tickers[x]], y=df[tickers[x]].shift(1),color="deepskyblue",alpha=0.5, ax=axes[i,j])

ax.set_title(tickers[x])

ax.set_xlabel("t")

ax.set_ylabel("t+1")

x = x + 1

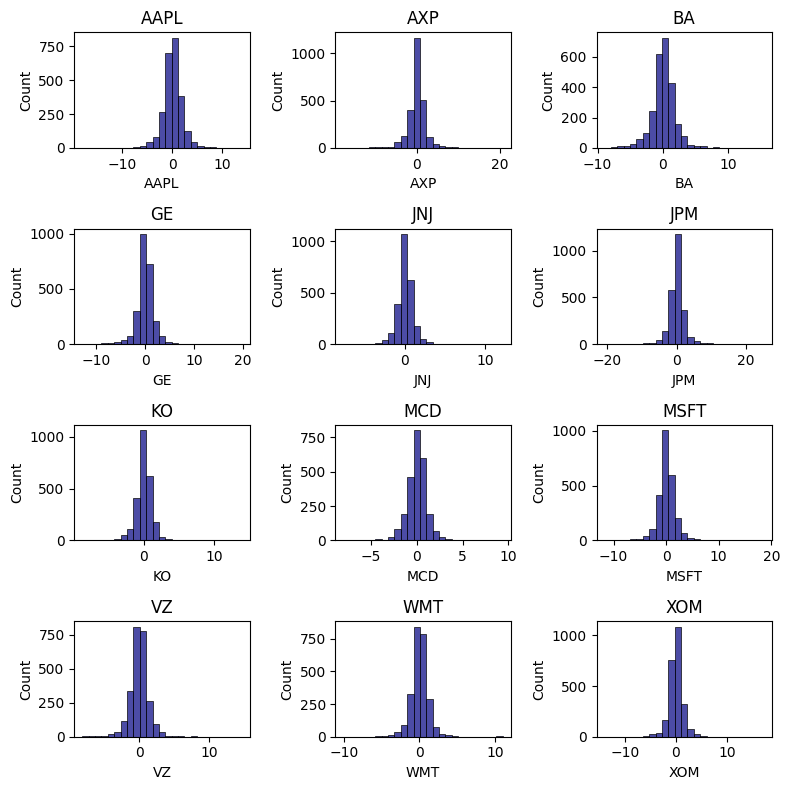

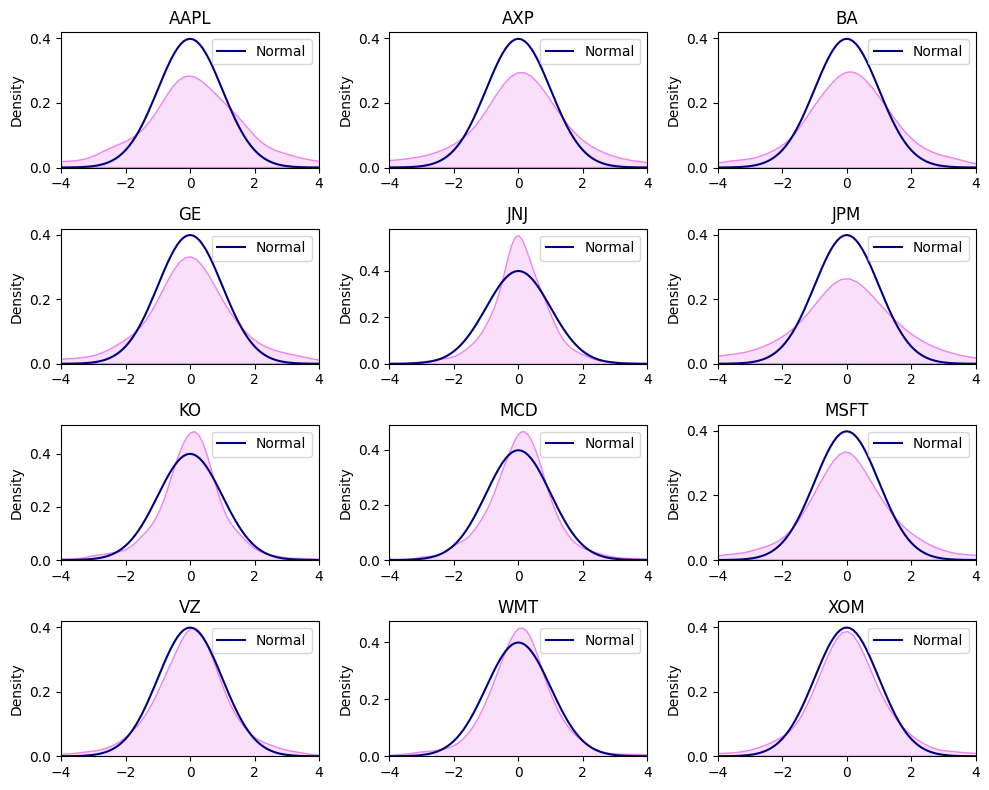

plt.tight_layout()The daily return on assets are collected and represented in the

form of histogram given in the figure below, from initial

analysis it seems that most of the stocks closely resemble

normal distribution. Most of these returns are

concentrated towards the mean value but a

small portion of these return are scattered at the end of the

distribution showing few days where there is large swing in

price

fig, axes = plt.subplots(nrows=4, ncols=3, figsize=(8,8))

tickers = df.columns

x = 0

for i in range(4):

for j in range(3):

ax = sns.histplot(df[tickers[x]], bins=25, color="navy", alpha=0.7, ax=axes[i,j])

ax.set_title(tickers[x])

x = x + 1

plt.tight_layout()

from scipy import stats

tickers = df.columns

xnor = np.arange(-10,10, 0.1)

ynor = stats.norm.pdf(xnor)

x = 0

fig, axes = plt.subplots(nrows=4, ncols=3, figsize=(10,8))

for i in range(4):

for j in range(3):

ax = sns.kdeplot(df[tickers[x]],color="violet", fill=True, ax=axes[i,j])

sns.lineplot(x=xnor, y=ynor, lw=1.5, color="navy", ax=axes[i,j], label="Normal")

ax.set_xlim(-4,4)

ax.set_title(tickers[x])

ax.set_xlabel("")

x = x + 1

plt.tight_layout()

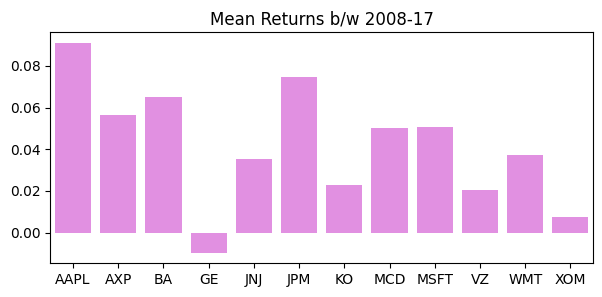

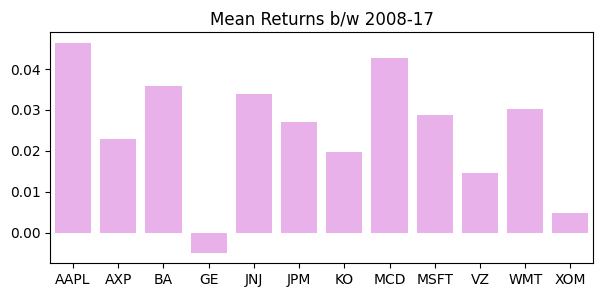

pd.DataFrame(df.mean(), columns=["MeanReturn"]).T| AAPL | AXP | BA | GE | JNJ | JPM | KO | MCD | MSFT | VZ | WMT | XOM | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| MeanReturn | 0.0910855 | 0.0565557 | 0.0651659 | -0.00971978 | 0.0352106 | 0.0744775 | 0.0229866 | 0.0500293 | 0.0505538 | 0.0202781 | 0.0371706 | 0.00742542 |

plt.figure(figsize=(7,3))

ax1 = sns.barplot(x=df.columns, y=df.mean(), color="violet")

ax1.set_title("Mean Returns b/w 2008-17");

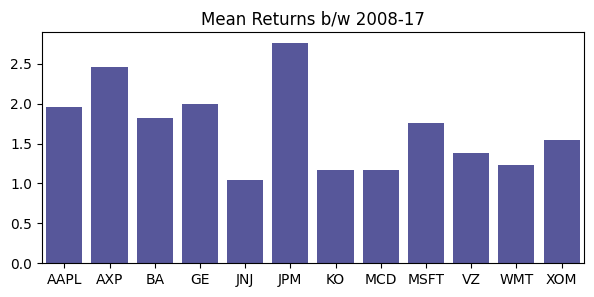

In the context of finance the risk can be defined as the

uncertainty in the market. Mathematically it can defined as

the deviation away from the expected

historical returns during a particular time period. A more

preferred definition in our context of our analysis is the

degree of making loss on a potential investment.There are

several statistical methods use to measure financial risk

Standard Deviation is the most commonly employed method for calculating financial risk. It can be expressed as.

$$sd_{asset} = \sqrt{\frac{\sum_(x_i - \mu)^2}{N}}$$

N is the total number of daily returns observed,

xi is daily observed return,

μ is mean return observed during N days.

The greater the Standard Deviation of the security

the more risky the asset is (in relative terms). The

Standard Deviation calculates the historical volatility of

the security, greater the dispersion from the

mean value indicates more volatile asset. From

the table we can observe that JNJ is least risky asset with standard

deviation of 1.0321% while JPM is the most risky asset with standard

deviation of 2.733%.

pd.DataFrame(df.std(), columns=["SD"]).T| AAPL | AXP | BA | GE | JNJ | JPM | KO | MCD | MSFT | VZ | WMT | XOM | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SD | 1.96343 | 2.46044 | 1.81769 | 1.99671 | 1.03731 | 2.75639 | 1.17105 | 1.17366 | 1.75271 | 1.38044 | 1.23344 | 1.54305 |

plt.figure(figsize=(7,3))

ax1 = sns.barplot(x=df.columns, y=df.std(), color="navy", alpha=0.7)

ax1.set_title("Mean Returns b/w 2008-17");

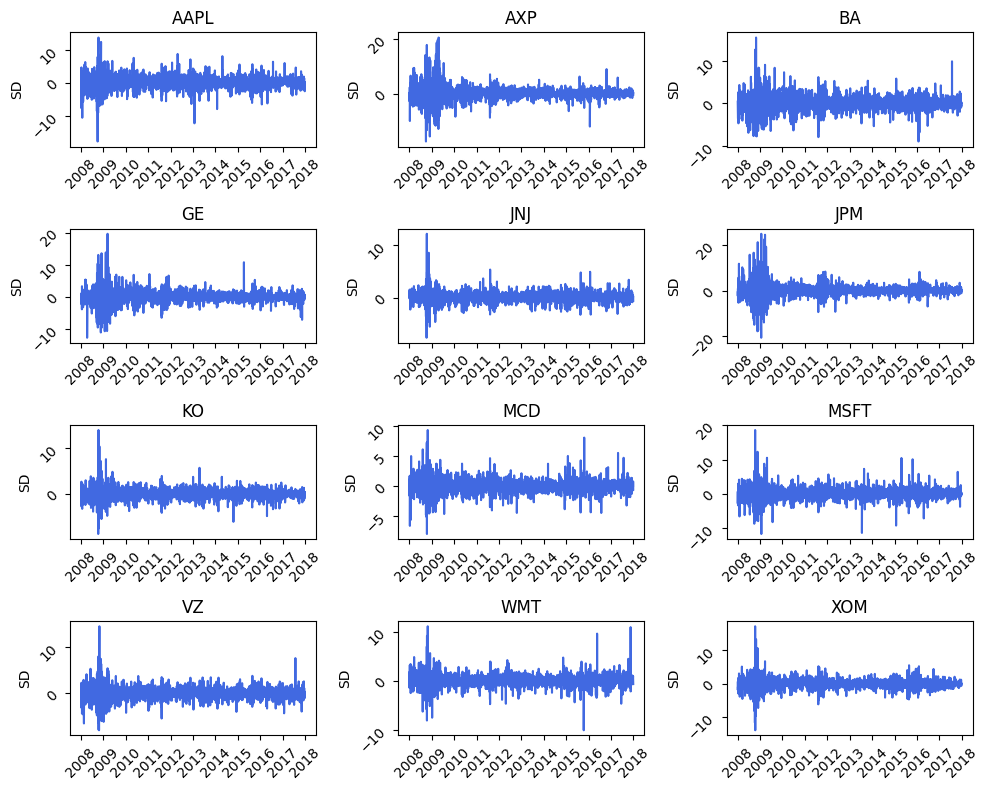

A more preferable method is using the

daily volatility clustering technique which helps in

visualizing the volatility at specific periods

in time.From Figure we can observe that the period between the year

2008 to 2010 was extremely volatile period due to rapid

change in the stock prices from their mean value, the contributing

factor for this rapid movement was in response to the

subprime mortgage crises in US due to which their was a

large scale financial panic in the market. After the

US government intervened in the financial markets to calm

down the rapid volatility in the market, the price movement

started to become less intense.

fig, axes = plt.subplots(nrows=4, ncols=3, figsize=(10,8))

tickers = df.columns

x = 0

for i in range(4):

for j in range(3):

ax = sns.lineplot(x=df.index, y=df[tickers[x]],color="royalblue",alpha=1, ax=axes[i,j])

ax.tick_params(labelrotation=45)

ax.set_title(tickers[x])

ax.set_xlabel("")

ax.set_ylabel("SD")

x = x + 1

plt.tight_layout()

Markowitz (1952) argued that the individual risk

pertaining to an asset is not as much important as the

contribution of risk from each asset to the

aggregate portfolio.In the financial markets only those

risk are compensated that cannot

be avoided.

In the financial market no two financial assets are either

completely correlated or completely independent of each other, to some

degree each asset is interrelated to the

movement of the prices of another asset , some assets have

very high degree of co-movement while some have less exposure to each

other. The Modern Portfolio Theory attempts to analyze the

interrelationship between different investments. It

utilizes statistical measures such as correlation to

quantify the diversification effect on portfolio

The extent to which the risk of the portfolio can be reduced

largely depends on the covariance between different assets.

Portfolio assets which have low correlation coefficients

are considered to be less risky than pairs with high

coefficients

Within the portfolio ofN assets there are N

variances and N(N-1) covariance. As the number of assets in

the portfolio increases the number of covariance increases

rapidly. This large number of covariance are very

importanttowards determining the risk of the

portfolio.

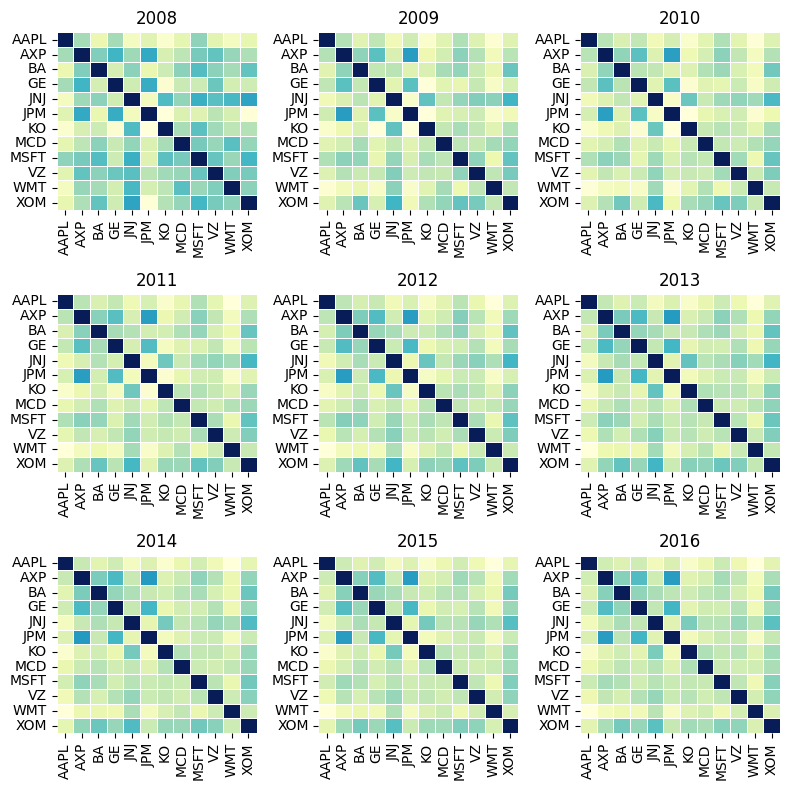

In the Figure we can observe that at the start of the year

2008 the correlation among the assets were

lowas the crises took of , the correlation

start to become stronger between the various

pairs of asset. In the year between 2009 and

2013 we can see a high correlation among the assets which

can be attributed to the increase in

systematic risk due to panic in the US

financial industry. After 2013 the correlation among the pairs of asset

start to decline due to decrease in systematic risk. During

the time of financial stress the correlation among the pairs of the

portfolio becomes very high due to intense

volatility in the market.

fig, axes = plt.subplots(nrows=3, ncols=3, figsize=(8,8))

periods =["2008-12-31", "2009-12-31","2010-12-31","2011-12-31","2012-12-31","2013-12-31","2014-12-31","2015-12-31","2016-12-31"]

x = 0

for i in range(3):

for j in range(3):

ax = sns.heatmap((df[:periods[x]].corr()), lw=0.5, cmap="YlGnBu", cbar=False, ax=axes[i,j])

ax.set_title(periods[x][:4])

x = x + 1

plt.tight_layout()

Sharpe ratio give insight to the investor what he is getting as a return on a security for the unit amount of risk he is taking. Sharpe ratio is calculated using

$${Sharpe Ratio} = \frac{R_{asset}-R_f}{\sigma_{assest}}$$

Rasset return on asset

Rf risk free rate

σasset SD of asset

Modern Portfolio theory sttes that adding assets to a portfolio

that have low correlation can decrease

portfolio risk without sacrificing the return. The

larger the sharpe ratio the

better it is for portfolio

pd.DataFrame(df.mean()/df.std(), columns=["Sharpe Ratio"]).T| AAPL | AXP | BA | GE | JNJ | JPM | KO | MCD | MSFT | VZ | WMT | XOM | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sharpe Ratio | 0.0463911 | 0.022986 | 0.035851 | -0.00486789 | 0.0339443 | 0.02702 | 0.019629 | 0.0426267 | 0.0288432 | 0.0146896 | 0.0301357 | 0.00481216 |

plt.figure(figsize=(7,3))

ax1 = sns.barplot(x=df.columns, y=df.mean()/df.std(), color="violet", alpha=0.7)

ax1.set_title("Mean Returns b/w 2008-17");

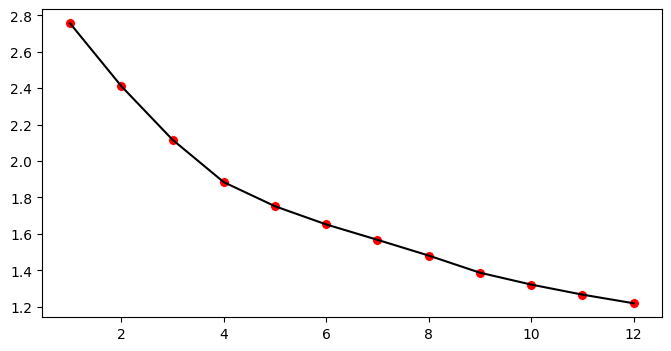

The effect of diversification is of central importance to Modern

Portfolio Theory. The process of diversification suggests the investor

to invest in multiple assets across different

asset classes and industries. As the number of securities in the

portfolio increases the portfolio become less

risk inherent.

But the decreases is non linear in

nature. As in the Figure we can observe that as the number of assets

increase (equal weighted portfolio) the standard deviation decreases at

a diminishing rate, after adding a certain number of assets

if we add more assets to the portfolio it does not have

much impact in decreasing the portfolio risk because some

risk will always remain in the form of systematic risk which cannot be

reduced.

dec_sd = df.std().sort_values(ascending=False).index

wport_sd =[]

for i in range(1,13):

equal_weight = np.repeat(1/i, i).reshape(-1,1)

covar = df.loc[:,dec_sd[:i]].cov().to_numpy()

sd = np.sqrt(np.dot(equal_weight.T,np.dot(covar, equal_weight)))

wport_sd.append(sd)

wport_sd = np.array(wport_sd).reshape(12,)plt.figure(figsize=(8,4))

sns.scatterplot(x=range(1,13), y=wport_sd, color="red", s=50, legend=False)

sns.lineplot(x=range(1,13), y=wport_sd, color="black", legend=False);

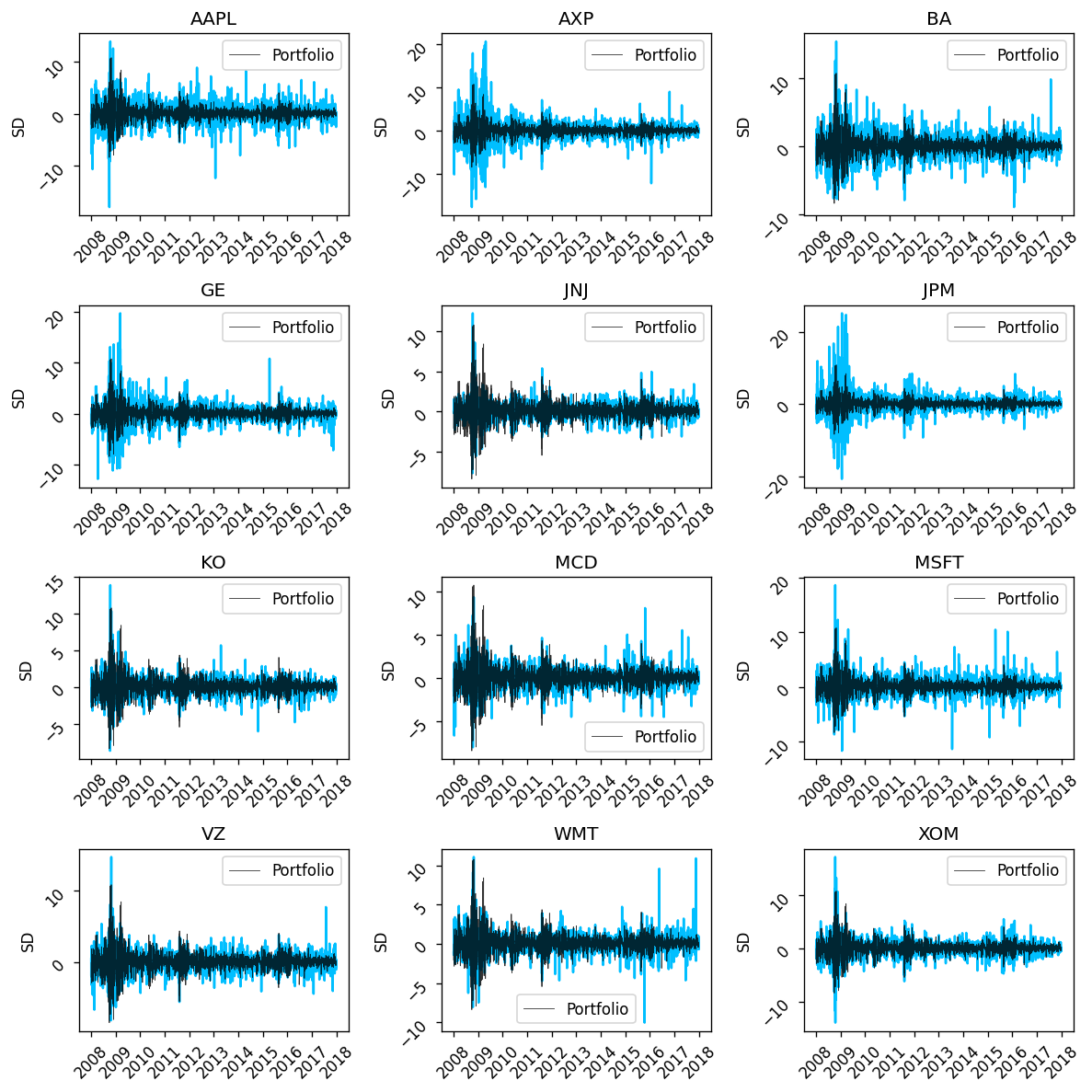

From Volatility clustering we can conclude that portfolio returns are much less volatile than any single stock return

dates = df.index

freq_assets = df.shape[1]

daily_returns = []

weight = np.repeat(1/freq_assets, freq_assets).reshape(-1,1)

for date in dates:

asset_return = df.loc[date].to_numpy()

port_return = np.dot(weight.T, asset_return)

daily_returns.append(port_return)portfolio_return = np.array(daily_returns).reshape(df.shape[0],)fig, axes = plt.subplots(nrows=4, ncols=3, figsize=(10, 10),dpi=120)

tickers = df.columns

x = 0

for i in range(4):

for j in range(3):

ax = sns.lineplot(x=df.index, y=df[tickers[x]],color="deepskyblue",alpha=1, ax=axes[i,j])

sns.lineplot(x=df.index, y=portfolio_return, color="black",linewidth=0.5, alpha=0.8, ax=axes[i,j], label="Portfolio")

ax.tick_params(labelrotation=45)

ax.set_title(tickers[x])

ax.set_xlabel("")

ax.set_ylabel("SD")

x = x + 1

plt.tight_layout()

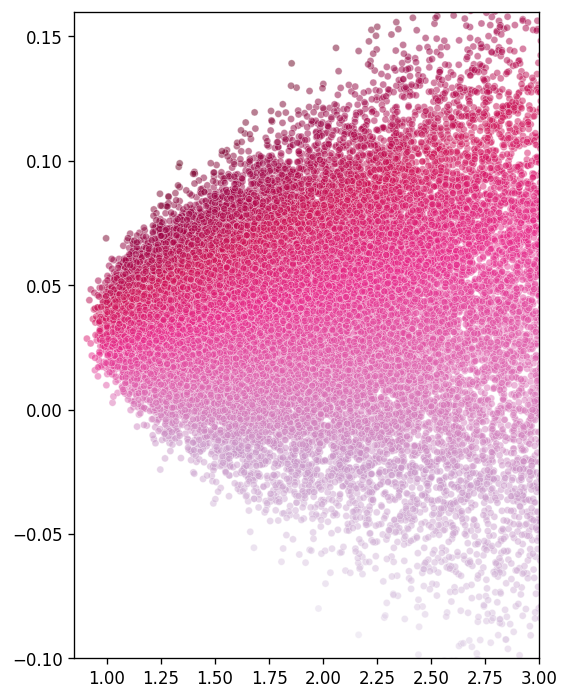

Markowitz concluded that out of infinite portfolio

that can be constructed by assigning different weights to

the portfolio (of the 12 stocks) there will be one

efficient portfolio which gives an investor

maximum return for a given amount of risk.

The investor would always prefer the portfolio over the

other inefficient portfolios because it maximizes his

utility

Using computer simulation we have generated more

than 50,000 randomly weighted portfolios out of the 12 stocks and

plotted their expected return and standard deviation.

From the Figure we can observe that these random portfolios

constitutes a parabolic curve. At the edge of

these curve lie the efficient portfolios which investor

prefer over other portfolios based on their

utility.

row = 50000

col = 12

random = np.random.normal(size=row*col).reshape(row,col)

sum_ = random.sum(axis=1)

weights = []

for idx in range(row):

weight = random[idx]/sum_[idx]

weights.append(weight)

weights = np.array(weights)mean = []

sd = []

covar = np.array(df.cov())

daily_mean = np.array(df.mean())

for idx in range(weights.shape[0]):

w = weights[idx].reshape(-1,1)

port_mean = np.dot(w.T,daily_mean)

port_sd = np.sqrt(np.dot(w.T, np.dot(covar,w)))

mean.append(port_mean)

sd.append(port_sd)

mean = np.array(mean).reshape(row,)

sd = np.array(sd).reshape(row,)

sharpe = mean/sdplt.figure(figsize=(5,7),dpi=120)

ax = sns.scatterplot(x=sd, y=mean, color="red", size= 2,alpha=0.5, hue=sharpe, palette="PuRd", legend=False)

ax.set_xlim(0.85,3)

ax.set_ylim(-0.1,0.16);